Small businesses are the backbone of the Indian economy, providing a significant portion of employment opportunities and contributing to the country’s GDP. However, a major challenge faced by these small business owners is access to credit. In response to this challenge, the Government of India launched the MUDRA (Micro Units Development and Refinance Agency) loan scheme in 2015. This article provides an overview of the Mudra Loan scheme, its features, benefits, and how it can empower small business owners in India.

What is MUDRA LOAN ?

MUDRA (Micro Units Development and Refinance Agency) loan is a scheme launched by the Government of India to provide financial assistance to small and micro-enterprises in the country. It is aimed at promoting entrepreneurship and creating employment opportunities in the small and micro-enterprise sector by providing collateral-free loans of up to Rs. 10 lakhs to eligible businesses. MUDRA loans are disbursed through various financial institutions such as banks, NBFCs, MFIs, and other lending institutions registered under the MUDRA scheme. The loans offered under the MUDRA scheme are categorized into three types, namely Shishu, Kishore, and Tarun, based on the funding requirements of the business. The scheme has been instrumental in providing financial support to millions of small business owners in India and has contributed significantly to the growth of the Indian economy.

What is e-mudra loan ?

E-mudra loan is a digital platform that enables small business owners to apply for MUDRA loans online. It is an initiative by the Government of India to promote digitalization and ease the loan application process for small business owners. Through the E-MUDRA portal, eligible applicants can apply for loans of up to Rs. 10 lakhs without the need for any physical documentation or collateral. The loan application process is entirely online and requires applicants to submit their basic personal and business details along with relevant documents. Once the application is processed and approved, the loan amount is disbursed directly to the applicant’s bank account. E-MUDRA loan has helped simplify the loan application process for small business owners and has made it more accessible and convenient for them to avail of financial assistance for their businesses.

What is Pradhan Mantri Mudra Yojana ?

Pradhan Mantri Mudra Yojana (PMMY) is a flagship scheme launched by the Government of India to provide financial assistance to small and micro-enterprises in the country. Under this scheme, eligible businesses can avail of collateral-free loans of up to Rs. 10 lakhs to start, expand, or modernize their operations. PMMY is a part of the MUDRA loan scheme and is aimed at promoting entrepreneurship and creating employment opportunities in the small and micro-enterprise sector.

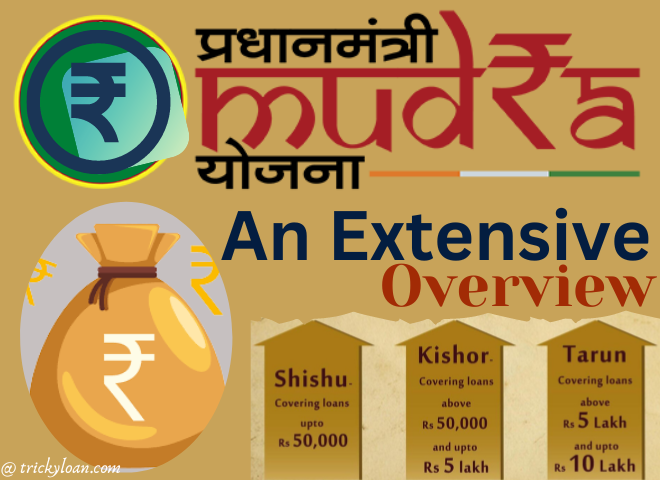

Types of MUDRA Loans

Under the MUDRA loan scheme, there are three types of loans available to micro and small business units:

1. Shishu Loan

Shishu loan is the smallest loan amount offered under the MUDRA scheme, with a maximum amount of Rs. 50,000. This loan is intended for small business owners who require a small amount of capital to start or expand their business.

2. Kishore Loan

Kishore loan is the medium-sized loan amount offered under the MUDRA scheme, with a maximum amount of Rs. 5 lakhs. This loan is intended for small business owners who require a larger amount of capital to expand their business.

3. Tarun Loan

Tarun loan is the largest loan amount offered under the MUDRA scheme, with a maximum amount of Rs. 10 lakhs. This loan is intended for small business owners who require a significant amount of capital to expand their business to the next level.

Features of MUDRA Loan

The following are the key features of the MUDRA loan scheme :-

- No Collateral Required

MUDRA loans are collateral-free, which means that small business owners do not have to pledge any assets as security to obtain a loan.

- Simplified Application Process

The application process for MUDRA loans is simple and straightforward. Small business owners can apply for the loan online or by visiting the nearest bank or financial institution.

- Quick Disbursement of Funds

MUDRA loans are disbursed quickly, usually within 7-10 working days from the date of approval of the loan application.

- Flexible Repayment Terms

MUDRA loans come with flexible repayment terms, with a repayment period of up to 5 years. Small business owners can choose to repay the loan in monthly, quarterly, or half-yearly installments.

- No Processing Fees

One of the key benefits of availing a MUDRA loan is that there are no processing fees charged to the borrower. This means that borrowers do not have to pay any charges for processing their loan application, making it more affordable and accessible for small business owners. The absence of processing fees makes it easier for small businesses to avail of financial assistance without worrying about additional expenses. However, it is important to note that some financial institutions may charge nominal processing fees, so borrowers should check with the lender before applying for a MUDRA loan. Nevertheless, the fact that the government has mandated no processing fees for MUDRA loans is a significant advantage for small businesses looking to secure funds for their growth and expansion.

- Interest Rates

The interest rates on MUDRA loans vary from bank to bank, and can range from 8% to 12% per annum.

- Loan Repayment

MUDRA loans are typically repaid in monthly installments over a period of 5 to 7 years, depending on the loan amount and the repayment capacity of the borrower.

Eligibility Criteria for MUDRA Loan

To be eligible for a MUDRA loan, an individual or business must meet certain criteria set by the government. Here are some of the key eligibility criteria for availing a MUDRA loan:

- Business Type

The business must be engaged in income-generating activities such as manufacturing, trading, and service sectors.

- Business Size

Small and micro-enterprises are eligible to apply for MUDRA loans. The business should have a turnover of up to Rs. 5 crores and a loan requirement of up to Rs. 10 lakhs.

- Age

The borrower should be between 18 and 65 years of age.

- Identity Proof

The borrower should have a valid identity proof such as Aadhaar card, PAN card, voter ID, or passport.

- Address Proof

The borrower should have a valid address proof such as Aadhaar card, passport, utility bill, or property tax receipt.

Business registration: The business should be registered with the relevant authorities such as GST, MSME, or any other regulatory body.

- Bank Account

The borrower should have a valid bank account in his or her name to receive the loan amount.

- Credit History

The borrower’s credit history should be good, with no default or overdue payments.

How to Apply for MUDRA Loan ?

The process of applying for a MUDRA loan is simple and straightforward. Here are the steps to follow:

- Identify the Type of MUDRA Loan

There are three types of MUDRA loans – Shishu, Kishore, and Tarun. Choose the type of loan that best suits your business needs.

- Prepare a Business Plan

A detailed business plan is required to apply for a MUDRA loan. The plan should outline the purpose of the loan, how the funds will be utilized, and the expected returns on investment.

- Approach a Financial Institution

Approach a bank or a financial institution that offers MUDRA loans. Submit your business plan and other necessary documents to the bank or financial institution.

- Fill out the Loan Application Form

The loan application form for a MUDRA loan is simple and can be filled out online or offline. Provide accurate information about your business and yourself in the application form.

- Submit the Required Documents

Along with the loan application form, submit the required documents such as identity proof, address proof, bank statements, business registration certificate, and others.

- Wait for Approval

Once the application is submitted, the bank or financial institution will evaluate the loan proposal and assess the creditworthiness of the borrower. If the application is approved, the loan amount will be disbursed to the borrower’s bank account.

Documents Required for MUDRA Loan

To apply for a MUDRA loan, borrowers need to provide the following documents:

- Identity Proof

Any government-issued document such as Aadhaar Card, PAN Card, Passport, or Voter ID.

- Address Proof

Any government-issued document such as Aadhaar Card, Utility Bill, Passport, or Voter ID.

- Business Registration Certificate

For businesses that are registered with the government, the registration certificate needs to be submitted.

- Bank Statement

The applicant needs to submit a bank statement for the last six months to establish the financial position of the business.

- Business Plan

A detailed business plan that outlines the objectives, operations, and financial projections of the business is required.

- Quotations and Invoices

If the loan is being taken to purchase machinery, equipment or raw materials, the borrower needs to provide quotations and invoices from suppliers.

- Other Documents

Depending on the loan amount and the type of business, the lender may require additional documents such as income tax returns, audited financial statements, and others.

It is important to note that the specific document requirements may vary based on the policies of the lender and the loan amount being applied for. It is advisable for borrowers to check with the lender regarding the specific documents needed for their loan application. By providing accurate and complete documents, borrowers can increase the chances of their loan application being approved.

Pradhan Mantri Mudra Yojana Application Form

The Pradhan Mantri Mudra Yojana (PMMY) application form can be obtained from any bank or financial institution that offers MUDRA loans. The form can also be downloaded from the official website of the Ministry of Finance or the MUDRA portal.

The application form for a MUDRA loan is simple and can be filled out online or offline. Here are the key details that need to be filled in the form:

- Personal Information

The applicant needs to provide personal information such as name, age, gender, and contact details.

- Business Information

The applicant needs to provide information about the business such as the name of the business, type of business, date of establishment, and the number of employees.

- Loan Details

The applicant needs to mention the loan amount required, the purpose of the loan, and the repayment period.

- Other Details

The applicant needs to provide details of the collateral security offered, if any, and the details of any existing loans.

Along with the application form, the applicant needs to submit the required documents such as identity proof, address proof, bank statements, business registration certificate, and others.

Once the application is submitted, the bank or financial institution will evaluate the loan proposal and assess the creditworthiness of the borrower. If the application is approved, the loan amount will be disbursed to the borrower’s bank account.

Interest Rates and Repayment Period for MUDRA Loan

The interest rate and repayment period for MUDRA loans depend on the type of loan and the policies of the lending institution. Here is a general overview:

- Shishu Loans

These are small loans of up to Rs. 50,000 and have an interest rate of around 12-15% per annum. The repayment period is up to 5 years, with a moratorium period of up to 6 months.

- Kishor Loans

These are medium-sized loans ranging from Rs. 50,000 to Rs. 5 lakhs and have an interest rate of around 14-17% per annum. The repayment period is up to 7 years, with a moratorium period of up to 12 months.

- Tarun Loans

These are larger loans ranging from Rs. 5 lakhs to Rs. 10 lakhs and have an interest rate of around 16-19% per annum. The repayment period is up to 10 years, with a moratorium period of up to 18 months.

It is important to note that these interest rates and repayment periods are subject to change based on the lending institution’s policies and the borrower’s creditworthiness. Additionally, lenders may also charge processing fees, prepayment charges, and other fees that can impact the total cost of the loan. Therefore, it is advisable for borrowers to carefully review the loan terms and conditions before applying for a MUDRA loan.

Benefits of MUDRA Loan

MUDRA loans offer several benefits to small business owners and entrepreneurs, including:

- Easy Accessibility

MUDRA loans are easily accessible and can be availed from several banks, NBFCs, and other financial institutions. This makes it easier for small business owners to access credit and expand their business operations.

- No Collateral Requirement

For most MUDRA loans, collateral is not required. This means that small business owners can apply for a loan without having to provide any security or assets as collateral.

- Low Interest Rates

MUDRA loans offer lower interest rates compared to other types of loans, making it more affordable for small business owners to borrow money.

- Flexible Repayment Terms

MUDRA loans offer flexible repayment terms, allowing small business owners to choose a repayment schedule that suits their business needs and cash flow.

- No Processing Fees

MUDRA loans do not have any processing fees, which makes it easier and more affordable for small business owners to access credit.

- Boosts Entrepreneurship

MUDRA loans aim to promote entrepreneurship and self-employment by providing financial assistance to small business owners and entrepreneurs. This can lead to job creation and economic growth in the long run.

- Encourages Financial Inclusion

MUDRA loans also promote financial inclusion by extending credit facilities to those who may not have access to formal banking channels. This helps to bridge the gap between the formal and informal sectors of the economy.

Challenges Faced by MUDRA Loan Scheme

While the MUDRA loan scheme has been successful in providing credit to small business owners and entrepreneurs, it has also faced some challenges. Some of these challenges include:

- Lack of Awareness

Despite the government’s efforts to promote the scheme, many small business owners and entrepreneurs are not aware of the MUDRA loan scheme and its benefits.

- Limited Reach

While the scheme is available across the country, its reach is limited to the areas where banks and financial institutions are present. This leaves out many small business owners who are located in remote areas and may not have access to formal banking channels.

- Delayed Disbursement

In some cases, the disbursement of MUDRA loans has been delayed due to the lengthy application process and the need for extensive documentation.

- Limited Loan Amounts

While MUDRA loans are intended for small business owners, the loan amounts offered may not be sufficient for some businesses to grow and expand.

- Lack of Credit History

Small business owners who do not have a credit history may face difficulties in obtaining a MUDRA loan due to the lack of a credit score or collateral.

- High Default Rates

Some small business owners who have availed MUDRA loans have defaulted on their repayments, leading to higher non-performing assets (NPAs) for banks and financial institutions.

- Limited Focus on Job Creation

While the MUDRA loan scheme aims to promote entrepreneurship and self-employment, it may not necessarily lead to job creation, which is a key challenge for the Indian economy.

Despite these challenges, the MUDRA loan scheme remains a valuable tool for small business owners and entrepreneurs looking to access credit and expand their business operations. The government and financial institutions must continue to address these challenges and work towards making the scheme more inclusive and effective.

Success Stories of MUDRA Loan

The MUDRA loan scheme has been instrumental in providing financial assistance to small business owners and entrepreneurs across the country. Here are some success stories of businesses that have benefitted from the scheme:

- Renuka Bhandare

Renuka is a farmer from Maharashtra who wanted to start her own dairy business. She applied for a MUDRA loan and received Rs. 5 lakhs to purchase cows and set up a dairy farm. Today, her business has grown significantly, and she employs several people from her village.

- Sandeep Kumar

Sandeep is a young entrepreneur from Haryana who started his own manufacturing business with the help of a MUDRA loan. He used the loan to purchase machinery and raw materials, and today his business has expanded to include several products that are sold across the country.

- Rajendra Singh

Rajendra is a weaver from Varanasi who wanted to expand his business but did not have the financial resources to do so. He applied for a MUDRA loan and received Rs. 3 lakhs, which he used to purchase new looms and raw materials. His business has since grown significantly, and he now employs several people from his village.

- Vijay Kumar

Vijay is a small business owner from Bihar who runs a grocery store. He applied for a MUDRA loan to expand his store and purchase additional inventory. With the loan, he was able to add new products and services, and his business has since grown significantly.

These success stories highlight the impact of the MUDRA loan scheme in promoting entrepreneurship and self-employment among small business owners and entrepreneurs. The scheme has helped many individuals access credit and start their own businesses, leading to job creation and economic growth in the country.

Impact of MUDRA Loan on the Indian Economy

The MUDRA loan scheme has had a significant impact on the Indian economy, particularly in terms of promoting entrepreneurship and self-employment. Here are some ways in which the scheme has impacted the economy:

- Job Creation

The MUDRA loan scheme has helped many individuals start their own businesses, leading to job creation and economic growth. According to a report by the Ministry of Finance, the scheme has led to the creation of over 7 crore jobs since its inception.

- Financial Inclusion

The scheme has helped promote financial inclusion by providing access to credit to small business owners and entrepreneurs who may not have had access to formal banking channels. This has helped to bridge the gap between the formal and informal economies.

- Promotion of Small Businesses

The scheme has helped promote the growth of small businesses by providing them with the financial resources they need to expand and grow. This has led to the development of a vibrant small business ecosystem in the country.

- Reduction in Dependence on Informal Sector

The MUDRA loan scheme has helped reduce dependence on the informal sector by providing small business owners with access to formal credit. This has helped to formalize many small businesses and bring them into the mainstream economy.

- Boost to GDP

The growth of small businesses, job creation, and financial inclusion facilitated by the MUDRA loan scheme have all contributed to a boost in the country’s GDP.

Comparison of MUDRA Loan with Other Schemes

The MUDRA loan scheme is one of several initiatives launched by the Indian government to promote entrepreneurship and small business development. Here’s a comparison of MUDRA loan with some other popular schemes:

- Stand-Up India

Stand-Up India is a scheme launched by the Indian government to promote entrepreneurship among women and SC/ST communities. It offers loans ranging from Rs. 10 lakh to Rs. 1 crore for setting up greenfield enterprises. While MUDRA loans also target small business owners and entrepreneurs, they do not have any specific focus on women or SC/ST communities.

- Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE)

The CGTMSE provides credit guarantees to small businesses and micro-enterprises. This means that banks can extend loans to these businesses without any collateral, as long as they meet certain eligibility criteria. While the MUDRA loan scheme also provides collateral-free loans to small businesses, it is not limited to micro-enterprises and has a higher loan limit.

- Startup India

Startup India is a government initiative aimed at promoting and supporting startups in India. It offers a range of benefits and incentives, such as tax exemptions and funding support. While MUDRA loans can also be availed by startups, they do not offer the same level of support as the Startup India scheme.

- Prime Minister’s Employment Generation Program (PMEGP)

PMEGP is a credit-linked subsidy scheme launched by the government to support micro-enterprises and small businesses. It offers a subsidy of up to 35% on the project cost, subject to certain limits. While both MUDRA loans and PMEGP aim to support small businesses, PMEGP offers a subsidy while MUDRA loans offer collateral-free loans.

Conclusion :-

Mudra loans are a great way for small and micro-enterprises to get the financial assistance they need to start or expand their businesses. With the easy application process and low-interest rates, mudra loans are an attractive option for entrepreneurs who need capital. If you fulfill the eligibility criteria, we recommend that you apply for a mudra loan and take advantage of this government scheme.

FAQs:

Q. What is the interest rate on mudra loans ?

A. The interest rate on mudra loans varies depending on the bank and the type of loan. However, the interest rate is usually lower than that of other commercial loans.

Q. Can I apply for multiple mudra loans ?

A. Yes, you can apply for multiple mudra loans, provided you fulfill the eligibility criteria and have the ability to repay the loan.

Q. Is collateral required for mudra loans ?

A. No, collateral is not required for mudra loans. However, the borrower must provide a personal guarantee.